International shipping can achieve 95%+ reductions in well-to-wake GHG emissions by 2050 with policy support, report shows

- nrehmatulla

- Nov 7, 2025

- 2 min read

Updated: Nov 26, 2025

Report from ERM, UMAS and UCL shows that international shipping can achieve 95%+ reductions in well-to-wake GHG emissions by 2050 with policy support

The report, commissioned by the UK Department for Transport as part of the evidence base for maritime decarbonisation policies, shows that international shipping can reach zero or very near zero tank-to-wake (TTW) CO2 emissions by 2050, and achieve 95%+ reductions in well-to-wake (WTW) GHG emissions from 2018 levels, in scenarios aligned to a 1.5°C global temperature goal. The report was published in April 2025 and is based on 2022 modelling using input data from the same year.

The study used the Global Maritime Transport Model to assess the relative costs and potential impacts of technology transitions within international shipping under three core scenarios. Scenario A makes steady reductions in TTW CO2 emissions starting from 2025, Scenario C delays until 2030 then makes rapid, deep cuts to achieve the same cumulative TTW CO2 emissions, whereas Scenario B makes rapid cuts from 2025-2035 to achieve 10% lower cumulative TTW CO2 emissions.

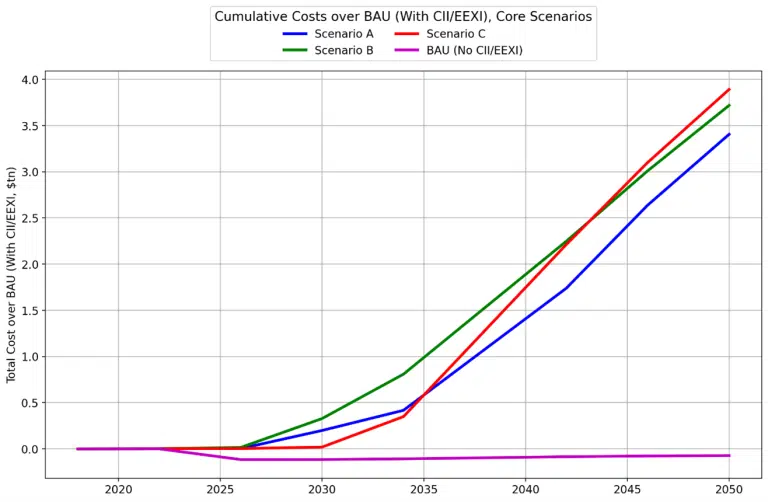

In all core scenarios, international shipping achieves zero or near-zero TTW CO2 emissions by 2050 at the latest, along with 95-98% reductions in WTW GHG emissions from 2018 levels. Figure 1 shows that cumulative costs vary – with each year of delay in the start of emission reductions, a further USD100bn is added to the total cost of decarbonisation. Delaying the start of shipping decarbonisation, even to 2030, results in a more disruptive change in technology, including greater scrappage of vessels, and a higher total cost for the transition.

The lowest total cost pathway involves the widespread use of low-carbon ammonia. There are other fuel options that could achieve a similar fleet decarbonisation outcome, such as low-carbon methanol and hydrogen, but at higher cost. In the core scenarios, demand for low-carbon ammonia grows rapidly from the end of the 2020s, and by the 2040s, it is the major fuel used in the shipping sector. To meet this level of ammonia demand, current global ammonia production capacity would need to quadruple by the 2040s, with year-on-year growth rates close to or exceeding historical record growth rates. This can only happen if action to unlock investment is taken urgently, which relies on rapid agreement of the underpinning policy frameworks.

The report highlights that the transition benefits from carefully designed policies. A combination of measures and the use of carbon revenues may be important. Moreover, policies that only focus on tank-to-wake (TTW) CO2 emissions can incentivise solutions such as Liquefied Natural Gas (LNG), which has significant upstream and non-CO2 GHG emissions. There is an urgent need to modify policy to use well-to-wake (WTW) GHG emissions, and increase policy stringency to accelerate the take-up of vessel efficiency measures.

The report and technical annex can be downloaded here: